{kind=link}

Earlier this year in January, the Reserve Bank of India’s flexible inflation targeting framework completed a decade as the primary determinant of Indian monetary policy. Informally adopted in January 2014 and officially in 2016, the framework has been the subject of considerable debate over the last few years.

There really are two branches to India’s inflation targeting debate: the numerical target—4% in a band of 2-6%, and the measure of inflation itself, which is headline inflation as measured by the consumer price index (CPI). The Economic Survey for 2023-24 has waded into this discussion, calling for a re-examination of the framework to see whether the target can be spelt out in terms of inflation excluding food.

The Survey makes a fairly compelling argument: food prices can’t really be countered by tools at the disposal of the monetary policy authority. Instead, it is the government that acts and helps cool these prices, which in turn “prevents farmers from benefiting from the rise in terms of trade in their favour”.

The Survey instead suggests that RBI focus on controlling inflation excluding food, leaving the government to take care of the hit to the pockets of the poor and low-income households from rising food prices through direct benefit transfers or even food coupons.

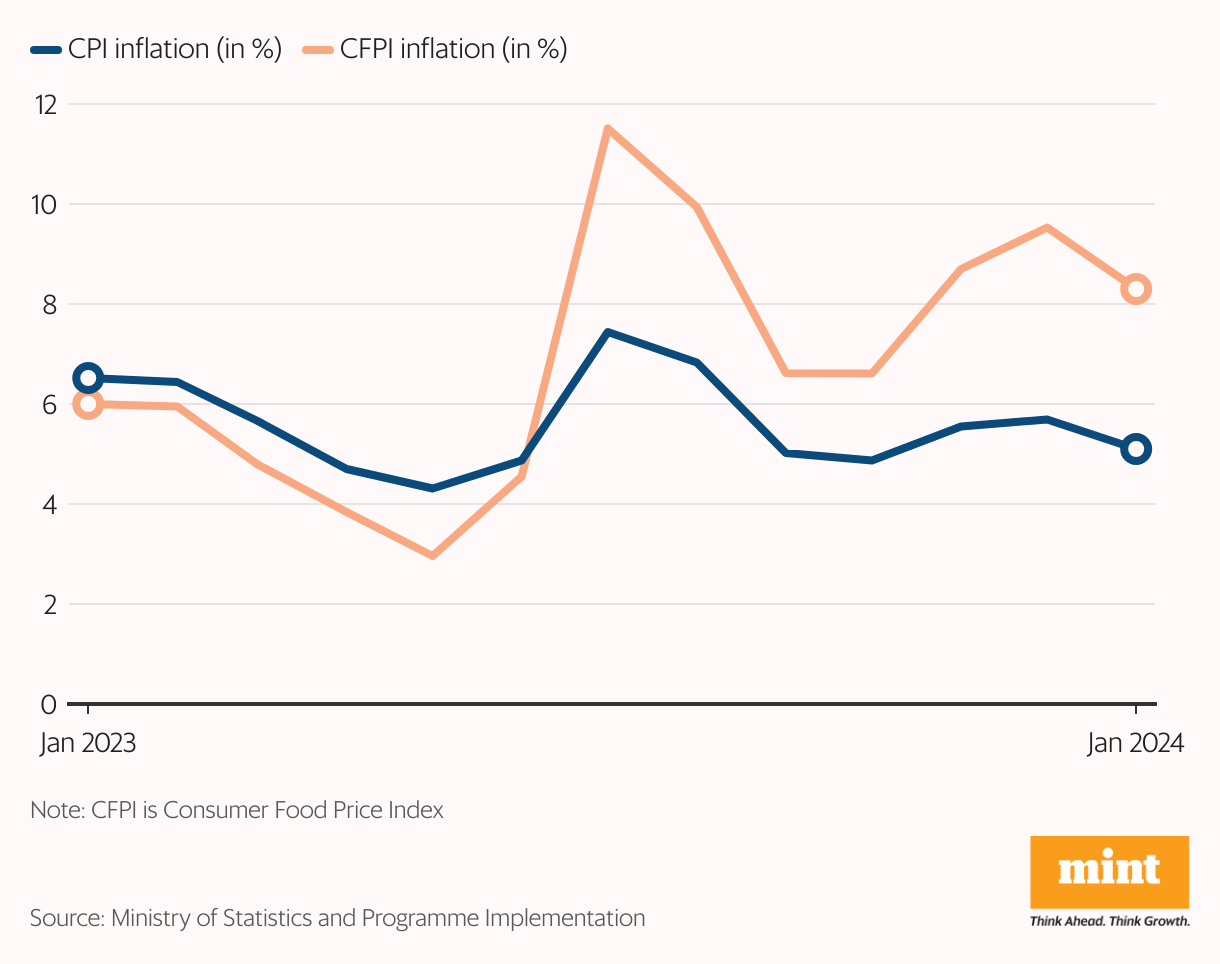

Given a choice, RBI would probably jump at the opportunity to not have to worry about food prices. Consider the last 10 months, which have seen CPI inflation average 5.1% and stay firmly within RBI’s target band of 2-6%.

At the same time, Consumer Food Price Inflation has averaged 8.4%, with the June print at a six-month high of 9.36%. No wonder RBI’s monetary policy committee (MPC) is focused on food prices and has left interest rates unchanged for eight meetings in a row.

There is, however, a problem in targeting non-food inflation. Had RBI been targeting this narrower measure of inflation, as suggested by the Economic Survey, its monetary policy actions would have looked very different from what we have seen.

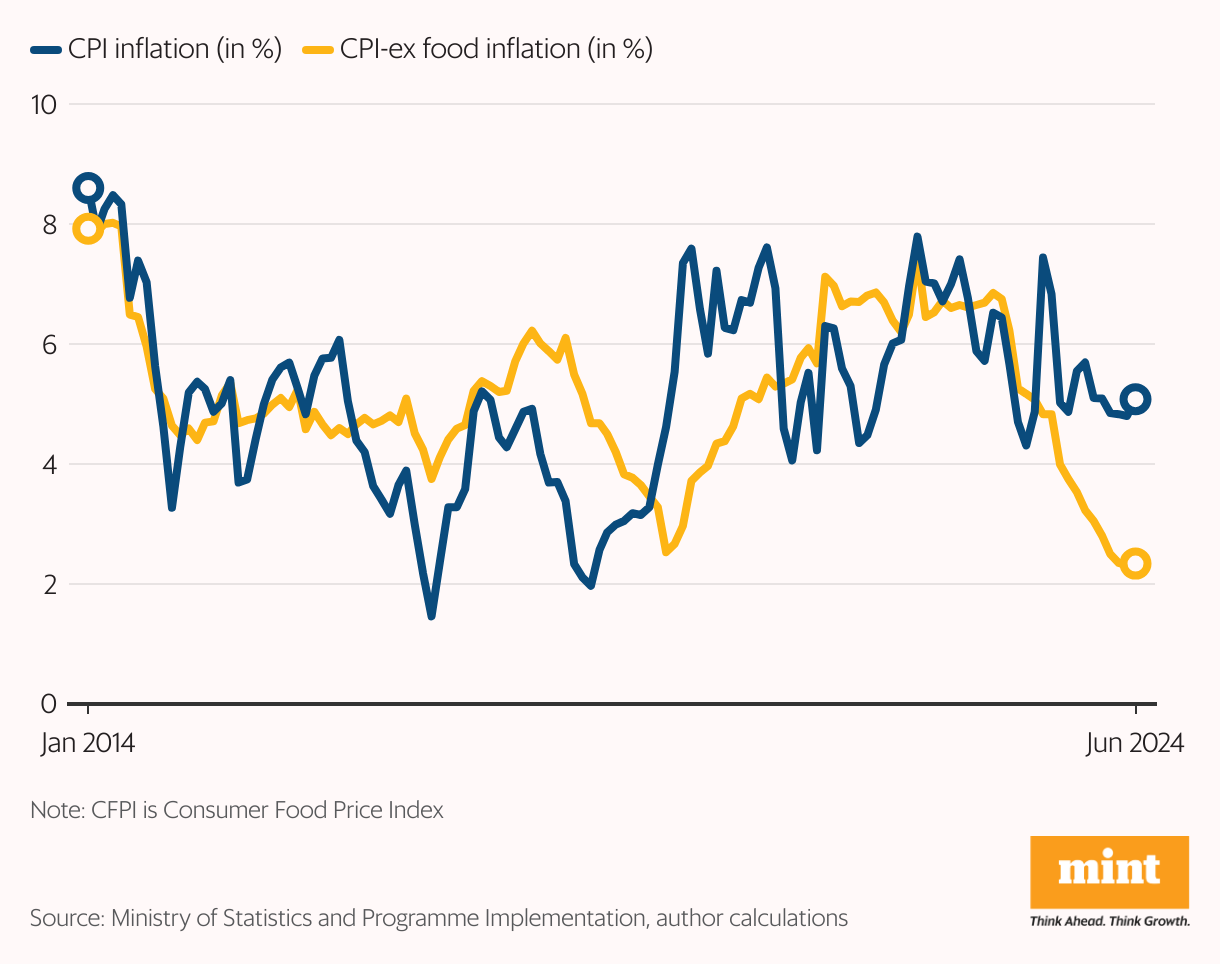

As per the law, the central bank is deemed to have failed when average CPI inflation is outside the 2-6% band for three quarters in a row. This occurred in 2022, when headline retail inflation averaged 6.3% in the January-March period, 7.3% in April-June, and 7.0% in July-September.

Once it started becoming clear that RBI was likely going to fail in its mandate, the MPC tightened the screws and began raising the policy repo rate starting in May 2022. The repo rate ended 2022-23 at 6.50%, 250 basis points higher than the pandemic-low of 4.00%.

If RBI was targeting non-food inflation, the central bank would have failed to meet its mandate in 2021 itself, with CPI inflation excluding food averaging 6.6% in April-June 2021, 6.7% in July-September, and 6.8% in October-December.

The central bank would have been forced to start its rate hike cycle a year earlier than it actually did, and economic growth may not have been as strong as it is now. Low food inflation of 3.1% in 2021, down from 9.6% in 2020, helped drag down the headline rate to a level that allowed India’s rate-setters to support growth amid the raging covid-19 pandemic.

To be sure, this is a hypothetical exercise. Further, headline inflation may not necessarily be the best target, with Ashima Goyal, one of the three external members on the MPC, having talked up the usefulness of core inflation—or inflation excluding food and fuel—as a policy anchor. However, even Goyal thinks “equity and consumer welfare considerations support targeting headline CPI”.

Nonetheless, the intervention by the Economic Survey comes at a rather opportune time. The current inflation target of 4% in a band of 2-6% is valid until March 2026. Coincidentally, it is expected that the ministry of statistics and programme implementation will release the new CPI inflation series, based on the latest Household Consumption Expenditure Survey, in early 2026.

The new inflation series should result in the weight of the ‘food and beverages’ group of the CPI reducing significantly from 45.86% at present; the same should hold true for the Consumer Food Price Index, which accounts for 39.06% of the CPI currently. This in itself should weaken the influence food prices exert over the headline inflation rate, making RBI’s job that much easier.

#Targeting #nonfood #inflation #doubleedged #sword #RBI